Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Key Skills You Need Your Listing Agent To Have

Selling your house is a big decision. And that can make it feel both exciting and a little bit nerve-wracking. However the key to a successful sale is finding the perfect listing agent to work with you throughout the process. A listing agent, also known as a seller’s agent, helps market and sell your house while advocating for you every step of the way.

But, how do you know you’ve found the perfect match in an agent? Here are three key skills you’ll want your listing agent to have.

The Price of Your House Based on the Latest Data

While it may be tempting to pick the agent who suggests the highest asking price for your house, that strategy may cost you. It’s easy to get caught up in the excitement when you see a bigger number, but overpricing your house can have consequences. It could mean it’ll sit on the market longer because the higher price is actually deterring buyers.

Instead, you want to pick an agent who’s going to have an open conversation about how they think you should price your house and why. A great agent will base their pricing strategy on solid data. They won’t throw out a number just to win your listing. Instead, they’ll show you the facts, explain their pricing strategy, and make sure you’re on the same page. As NerdWallet explains:

“An agent who recommends the highest price isn’t always the best choice. Choose an agent who backs up the recommendation with market knowledge.”

They’re a Great Negotiator

Home selling can be emotional, especially if you’ve been in your house for a long time. You’re connected to it and have a lot of memories there. This can make the negotiation process harder. That’s where a trusted professional comes in.

A skilled listing agent will be calm under pressure and will be your point person in all of those conversations. Their experience in handling the back-and-forth gives you with the peace of mind that you’ve got someone on your side who’s got your best interests in mind throughout this journey.

They’re a Skilled Problem Solver

At the heart of it all, a listing agent’s main priority is to get your house sold. A great agent never loses sight of that goal and will help you prioritize your needs above all else. If they identify any necessary steps you need to take, they’ll be open with you about it. Their commitment to your success means they’ll work with you to address any potential roadblocks and find creative solutions to anything that pops up.

BankRate explains it like this:

“Just as important as the knowledge and experience agents bring is their ability to guide you smoothly through the process. Above all, go with an agent you trust and will feel comfortable with. . .”

Bottom Line

Whether you’re a first-time seller or you’ve been through selling a house before, a great listing agent is the key to success. Connect with a real estate professional so you have a skilled local expert by your side to guide you through every step of the process.

Selling your house is a big decision. And that can make it feel both exciting and a little bit nerve-wracking. However the key to a successful sale is finding the perfect listing agent to work with you throughout the process. A listing agent, also known as a seller’s agent, helps market and sell your house while advocating for you every step of the way.

But, how do you know you’ve found the perfect match in an agent? Here are three key skills you’ll want your listing agent to have.

Why Your House Didn’t Sell

If your listing expired and your house didn’t sell, you’re likely feeling a little frustrated. Not to mention, you’re also probably wondering what went wrong. Here are three questions to think about as you figure out what to do next.

Did You Limit Access to Your House?

One of the biggest mistakes you can make when selling your house is restricting the days and times when potential buyers can tour it. Being flexible with your schedule is important when you’re selling your house, even though it might feel a bit stressful to drop everything and leave when buyers want to see it. After all, minimal access means minimal exposure to buyers. ShowingTime advises:

“. . . do your best to be as flexible as possible when granting access to your house for showings.”

Sometimes, the most determined buyers might come from far away. Since they’re traveling to see your house, they may not be able to change their plans easily if you only offer limited times for showings. So, try to make your house available as much as you can to accommodate them. It’s simple. If no one’s able to look at it, how’s it going to sell?

Did You Make Your House Stand Out?

When selling your house, the old saying matters: you never get a second chance to make a first impression. Putting in the work to make the exterior of your home look nice is just as important as how you stage it inside. Freshen up your landscaping to improve your home’s curb appeal so you can make an impact upfront. As an article from U.S. News says:

“After all, if people drive by, but aren’t interested enough to walk through the front door, you’ll never sell your house.”

But don’t let that impact stop at the front door. By removing personal items and reducing clutter inside, you give buyers more freedom to picture themselves in the home. Additionally, a new coat of paint or cleaning the floors can go a long way to freshening up a room.

Did You Price Your House Compellingly?

Setting the right price is extremely important when you’re selling your house. Even though it might feel tempting to push the price higher to maximize your profit, overpricing can scare away buyers and make it hard to sell quickly. Business Insider notes:

“. . . the biggest mistake sellers make is overpricing their home.”

If your house is priced higher than others like it, it could make buyers lose interest. Pay attention to the feedback people give your agent during open houses and showings. If lots of people are saying the same thing, it might be a good idea to think about lowering the price.

For all these insights and more, rely on a trusted real estate agent. A great agent will offer expert advice on relisting your house with effective strategies to get it sold.

Bottom Line

It’s natural to feel disappointed when your listing has expired and your house didn’t sell. Talk to a trusted real estate agent to figure out what happened and what to reconsider or change if you want to get your house back on the market.

Planning to Retire? Your Equity Can Help You Make a Move

Retiring is a significant milestone in life, bringing with it a lot of change and new opportunities. As the door to this exciting chapter opens, one thing you may be considering is selling your house and finding a home better suited for your evolving needs.

Fortunately, you may be in a better position to make a move than you realize. Here are a few reasons why.

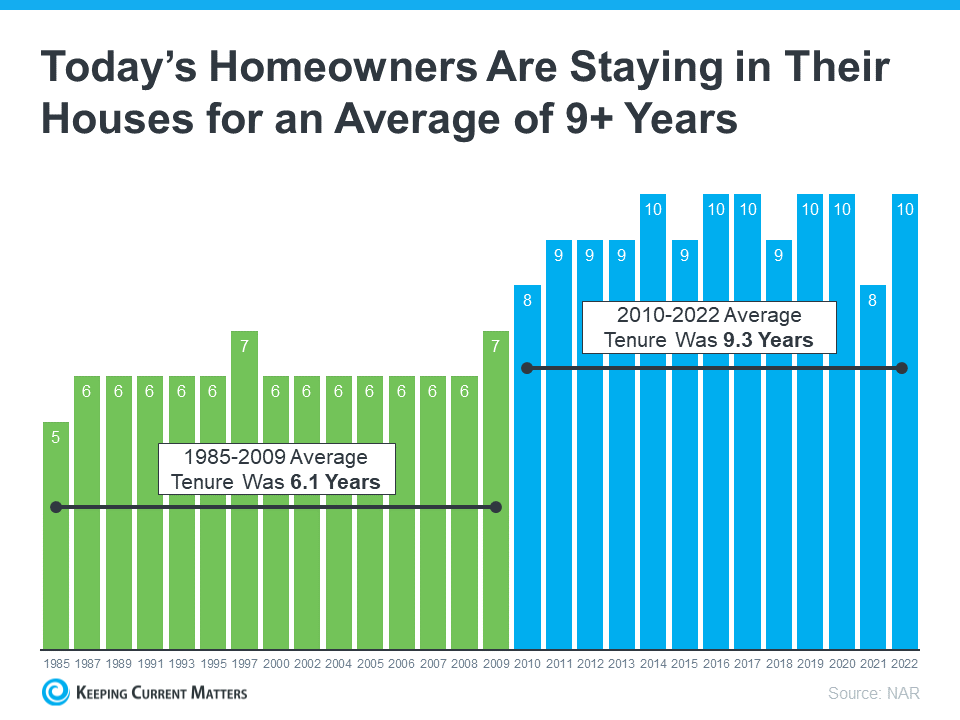

Consider How Long You’ve Been in Your Home

From 1985 to 2009, the average length of time homeowners stayed in their homes was roughly six years. But according to the National Association of Realtors (NAR), that number is higher today. Since 2010, the average home tenure is just over nine years (see graph below):

This means many homeowners have been living in their houses even longer in recent years. When you live in a home for such a significant amount of time, it’s natural for you to experience changes in your life while you’re in that house. As those life changes and milestones happen, your needs may change. And if your current home no longer meets them, you may have better options.

Consider the Equity You’ve Gained

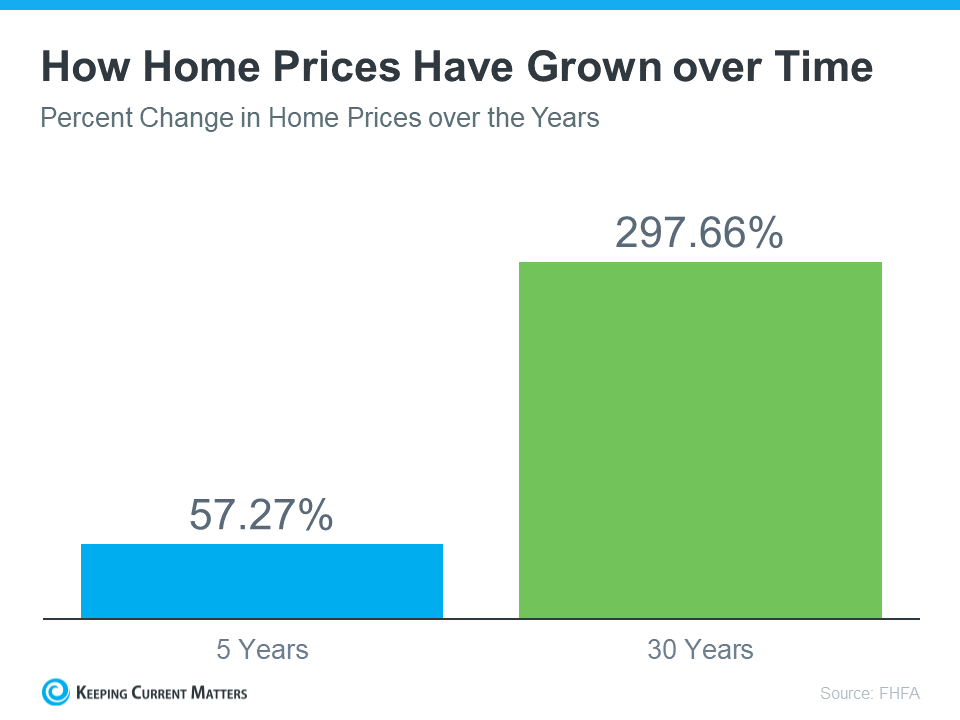

And, if you’ve been in your home for more than a few years, you’ve likely built up substantial equity that can fuel your next move. That’s because you gain equity as you pay down your loan and as home prices appreciate. And, the longer you’ve been in your home, the more you may have gained. Data from the Federal Housing Finance Agency (FHFA) illustrates that point (see graph below):

While home prices vary by area, the national average shows the typical homeowner who’s been in their house for five years saw it increase in value by nearly 60%. And the average homeowner who’s owned their home for 30 years saw it almost triple in value over that time.

Whether you’re looking to downsize, relocate to a dream destination, or move so you live closer to friends or loved ones, that equity can help. Whatever your home goals are, a trusted real estate agent can work with you to find the best option. They’ll help you sell your current house and guide you as you buy the home that’s right for you and your lifestyle today.

Bottom Line

As you plan for your retirement, connect with a local real estate agent to find out how much equity you’ve built up over the years and plan how you can use it toward purchasing a home that fits your changing needs.

Your Home Equity Can Offset Affordability Challenges

Are you thinking about selling your house? If so, today’s mortgage rates may be making you wonder if that’s the right decision. Some homeowners are reluctant to sell and take on a higher mortgage rate on their next home. If you’re worried about this too, know that even though rates are high right now, so is home equity. Here’s what you need to know.

Bankrate explains exactly what equity is and how it grows:

“Home equity is the portion of your home that you’ve paid off and own outright. It’s the difference between what the home is worth and how much is still owed on your mortgage. As your home’s value increases over the long term and you pay down the principal on the mortgage, your equity stake grows.”

In other words, equity is how much your home is worth now, minus what you still owe on your home loan.

How Much Equity Do Homeowners Have Now?

Recently, your equity has been growing faster than you might think. To help contextualize just how much the average homeowner has, CoreLogic says:

“. . . the average U.S. homeowner now has about $290,000 in equity.”

That’s because, over the past few years, home prices went up significantly – and those rising prices helped your equity to accumulate faster than usual. While the market has started to normalize, there are still more people wanting to buy homes than there are homes available for sale. This high demand is causing home prices to go up again.

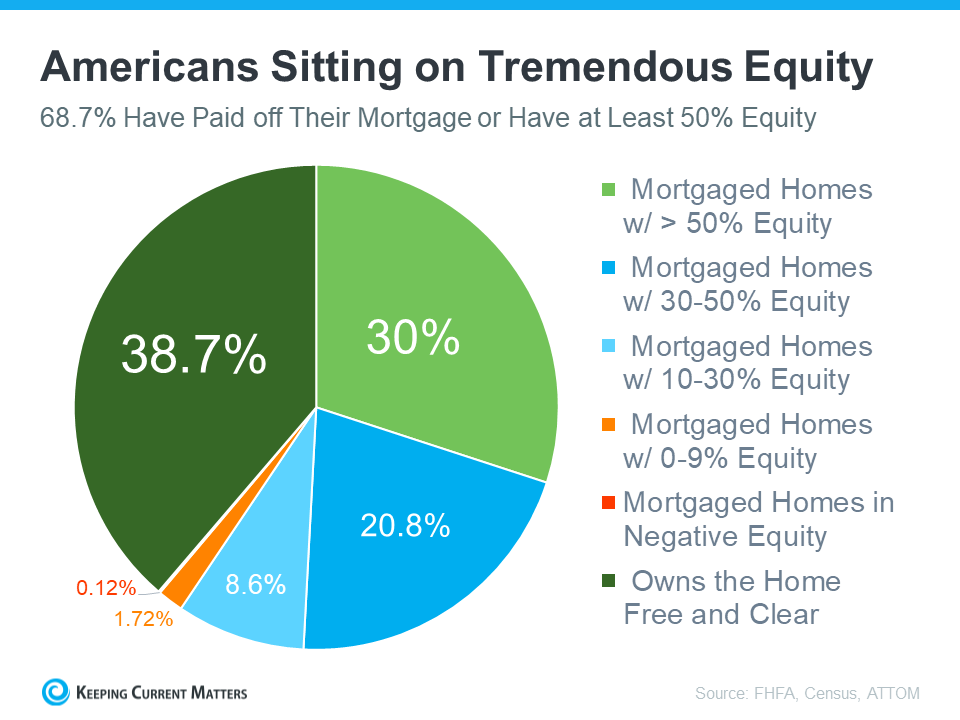

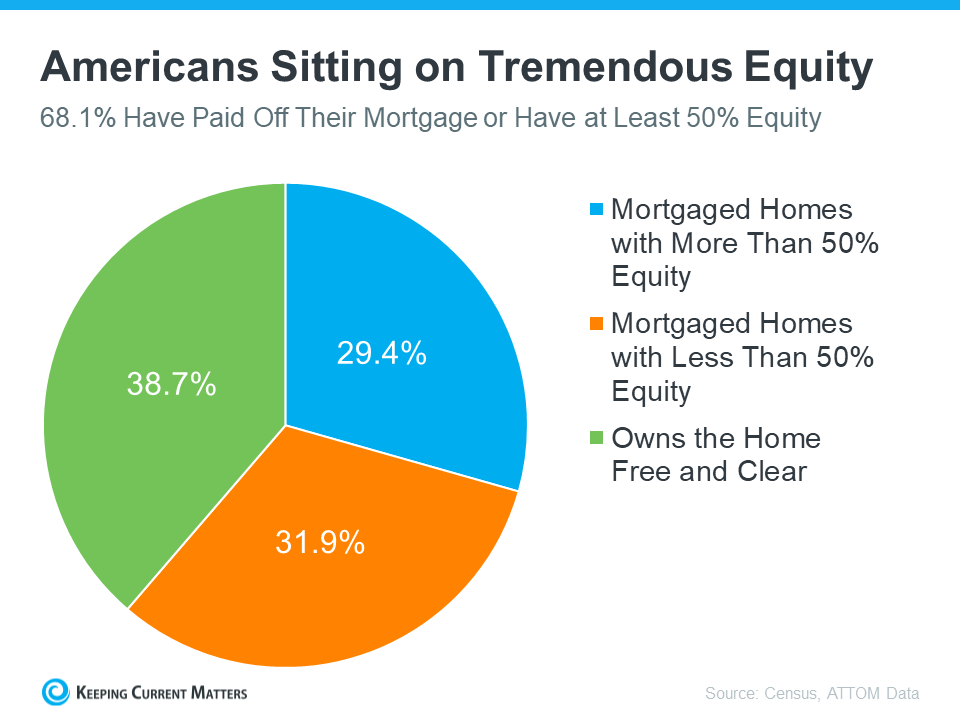

According to the Federal Housing Finance Agency (FHFA), the Census, and ATTOM, a property data provider, nearly two-thirds (68.7%) of homeowners have either fully paid off their mortgages or have at least 50% equity (see chart below):

That means nearly 70% of homeowners have a tremendous amount of equity right now.

How Equity Helps with Your Affordability Concerns

With today’s affordability challenges, your equity can make a big difference when you decide to move. After you sell your house, you can use the equity you’ve built up in your home to help you buy your next one. Here’s how:

- Be an all-cash buyer: If you’ve been living in your current home for a long time, you might have enough equity to buy a new house without having to take out a loan. If that’s the case, you won’t need to borrow any money or worry about mortgage rates. The National Association of Realtors (NAR) states:

“These all-cash home buyers are happily avoiding the higher mortgage interest rates . . .”

- Make a larger down payment: Your equity could be used toward your next down payment. It might even be enough to let you put a larger amount down, so you won’t have to borrow as much money so today’s rates become less of a sticking point. Experian explains:

“Increasing your down payment lowers your principal loan amount and, consequently, your loan-to-value ratio, which could lead to a lower interest rate offer from your lender.”

Bottom Line

If you’re thinking about moving, the equity you’ve built up can make a big difference, especially today. To find out how much equity you’ve got in your current house and how you can use it for your next home, get in touch with a trusted real agent.

Why It’s Still a Seller’s Market Today

Even though activity in the housing market has slowed from the frenzy that was the ‘unicorn’ years, it’s still a seller’s market because the supply of homes for sale is so low. But what does that really mean for you? And why are conditions today so good if you want to sell your house?

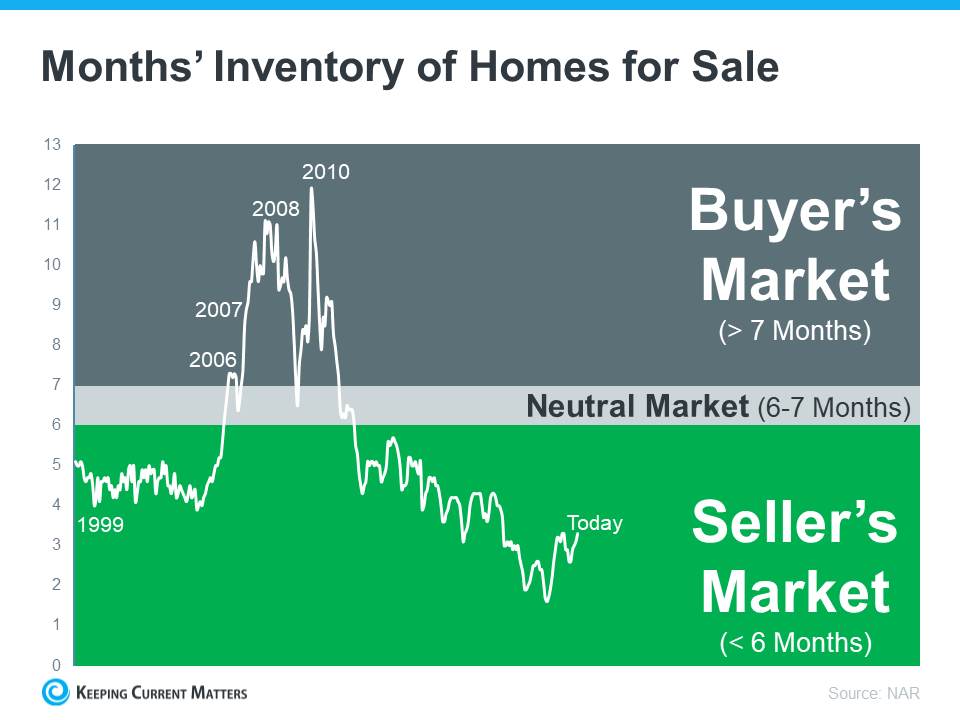

The latest Existing Home Sales Report from the National Association of Realtors (NAR) shows housing supply is still astonishingly low. Housing inventory is measured by the number of available homes on the market. It’s also measured by months’ supply, meaning the number of months it would take to sell all those available homes based on current demand. In a balanced market, there’s usually about a six-month supply. Today, we have only about 3 months’ supply of homes at the current sales pace (see graph below):

As the visual shows, given the current inventory of homes, it’s still a seller’s market.

Today, we’re nowhere near what’s considered a balanced market. In fact, the current month’s supply is half of what’s typical of a normal market. That means there just aren’t enough homes to go around based on today’s buyer demand.

As Lawrence Yun, Chief Economist for NAR, says:

“There are simply not enough homes for sale. The market can easily absorb a doubling of inventory.”

How Does Being in a Seller’s Market Benefit You?

Sellers, these conditions give you a real edge. Right now, there are buyers who are ready, willing, and able to purchase a home. And, because there’s a shortage of homes up for sale, the ones that do hit the market are like magnets for those buyers.

If you work with a local real estate agent to list your house right now, in good condition, and at the right price, it could get a lot of attention. You might even end up with multiple offers.

Bottom Line

Today’s seller’s market sets you up with a big advantage when you sell your house. Because supply is so low, your house will be in the spotlight for motivated buyers who are craving more options. Connect with a local real estate agent so you understand what’s happening in your area as you get ready to enter the market.

Leverage Your Equity When You Sell Your House

One of the benefits of being a homeowner is that you build equity over time. That equity can be used toward purchasing your next home by selling your house. But before you can put it to use, you should understand exactly what equity is and how it grows. Bankrate explains it like this:

“Home equity is the portion of your home you’ve paid off – in other words, your stake in the property as opposed to the lender’s. In practical terms, home equity is the appraised value of your home minus any outstanding mortgage and loan balances.”

Majority of Americans Have a Large Amount of Equity

If you’ve owned your home for a while, you’ve likely built up some equity – and you may not even realize how much. Based on data from the U.S. Census Bureau and ATTOM, the majority of Americans have a substantial amount of equity right now (see graph below):

And having such large amounts of equity benefits homeowners in more ways than one. Rick Sharga, Executive Vice President of Market Intelligence at ATTOM, explains:

“Record levels of home equity provide security for millions of families, and minimize the chance of another housing market crash like the one we saw in 2008.”

Over time, your home equity grows. In addition to providing financial stability while you own your house, when you’re ready to sell it, that money could go a long way toward paying for your next home.

Bottom Line

By selling your house and leveraging your equity, paying for your next home can be easier. Connect with a trusted real estate advisor so you can find out how much home equity you have and start planning your next move.

Why You Need a True Expert in Today’s Housing Market

The housing market continues to shift and change, and in a fast-moving landscape like we’re in right now, it’s more important than ever to have a trusted real estate agent on your side. Whether you’re buying your first home or selling once again, it’s mission-critical to work with an expert who can guide you through each unique step of the process.

The reality is, that not all agents operate the same way. To truly make a powerful and confident decision as you buy or sell a home, you need a real estate expert who uses their knowledge of what’s happening with home prices, housing supply, industry projections, and more to give you the best possible advice. Someone who can provide clarity and trust like that is essential to your success. Jay Thompson, Real Estate Industry Consultant, explains:

“Housing market headlines are everywhere. Many are quite sensational, ending with exclamation points or predicting impending doom for the industry. Clickbait, the sensationalizing of headlines and content, has been an issue since the dawn of the internet, and housing news is not immune to it.”

Unfortunately, when information in the media isn’t clear, it can generate a lot of fear and uncertainty for consumers. As Jason Lewris, Co-Founder and Chief Data Officer at Parcl, says:

“In the absence of trustworthy, up-to-date information, real estate decisions are increasingly being driven by fear, uncertainty, and doubt.”

But it doesn’t have to be that way. Buying a home is a big decision, and it should be one you feel confident making. You can lean on an expert to help you separate fact from fiction and get the answers you need.

The right agent can assist you in figuring out what’s going on at the national level and in your local area. They can debunk headlines using data you can trust. Experts have in-depth knowledge of the industry and can provide context, so you know how current trends compare to the normal ebbs and flows in the housing market, historical data, and more.

Then, to make sure you have the full picture, an agent can tell you if your local area is following the national trend or if they’re seeing something different in your market. Together, you can use all that information to make the best possible decision.

After all, making a move is a potentially life-changing milestone. It should be something you feel ready for and excited about. And that’s where a trusted expert comes in.

Bottom Line

If you want sound advice and trusted information about the housing market, reach out to a local real estate professional today.

About 11,000 Houses Will Sell Today

Some homeowners have been waiting for months to put their houses on the market because they don’t think people are buying homes right now. If that’s you, know that even though the housing market has slowed compared to the frenzy of a couple of years ago, it isn’t at a standstill. Contrary to what you may believe, buyers are still active and plenty of homes are selling right now.

According to the National Association of Realtors (NAR), based on the pace of sales right now, just over 4 million homes will sell this year. With some simple math, let’s break down what that really means for you:

- 4.16 million homes divided by 365 days in a year = 11,397 houses sell each day

- 11,397 divided by 24 hours in a day = 475 houses sell per hour

- 475 divided by 60 minutes in an hour = about 8 houses sell each minute

So, on average, about 11,000 homes sell each day in this country.

A real estate expert can give you more information about how many houses are being sold in your neighborhood, the amazing advantages that sellers are experiencing right now, and the most important things buyers are searching for in your area. Together you’ll use this knowledge to shape how you market your house based on local trends.

Bottom Line

If you’ve been waiting to sell because you don’t think there are buyers out there, know today’s market is active. Every day you wait, around 11,000 other homeowners are selling. In the time it took you to read this, eight homes sold. When you’re ready to sell too, connect with a local real estate agent.

Sellers: Don’t Let These Two Things Hold You Back

Many homeowners thinking about selling have two key things holding them back. That’s feeling locked in by today’s higher mortgage rates and worrying they won’t be able to find something to buy while supply is so low. Let’s dive into each challenge and give you some helpful advice on how to overcome these obstacles.

Challenge #1: The Reluctance to Take on a Higher Mortgage Rate

According to the Federal Housing Finance Agency (FHFA), the average interest rate for current homeowners with mortgages is less than 4% (see graph below):

But today, the typical 30-year fixed mortgage rate offered to buyers is closer to 7%. As a result, many homeowners are opting to stay put instead of moving to another home with a higher borrowing cost. This is a situation known as the mortgage rate lock-in effect.

But today, the typical 30-year fixed mortgage rate offered to buyers is closer to 7%. As a result, many homeowners are opting to stay put instead of moving to another home with a higher borrowing cost. This is a situation known as the mortgage rate lock-in effect.

The Advice: Waiting May Not Pay Off

While experts project mortgage rates will gradually fall this year as inflation cools, that doesn’t necessarily mean you should wait to sell. Mortgage rates are notoriously hard to predict. And, right now home prices are back on the rise. If you move now, you’ll at least beat rising home prices when you buy your next home. And, if experts are right and rates fall, you can always refinance later if that happens.

Challenge #2: The Fear of Not Finding Something to Buy

When so many homeowners are reluctant to take on a higher rate, fewer homes are going to come onto the market. That’s going to keep inventory low. As Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), explains:

“Inventory will remain tight in the coming months and even for the next couple of years. Some homeowners are unwilling to trade up or trade down after locking in historically-low mortgage rates in recent years.”

Even though you know this limited housing supply helps your house stand out to eager buyers, it may also make you feel hesitant to sell because you don’t want to struggle to find something to purchase.

The Advice: Broaden Your Search

If fear you won’t be able to find your next home is the primary thing holding you back, remember to consider all your options. Looking at all housing types including condos, townhouses, and even newly built homes can help give you more to choose from. Plus, if you’re able to work fully remote or hybrid, you may be able to consider areas you hadn’t previously searched. If you can look further from your place of work, you may have more affordable options.

Bottom Line

Instead of focusing on the challenges, focus on what you can control. Let’s connect so you’re working with a professional who has the experience to navigate these waters and find the perfect home for you.

Pricing Your House Right Still Matters Today

While this isn’t the frenzied market we saw during the ‘unicorn’ years, homes that are priced right are still selling quickly and seeing multiple offers right now. That’s because the number of homes for sale is still so low. Data from the National Association of Realtors (NAR) shows 76% of homes sold within a month and the average saw 3.5 offers in June.

To set yourself up to see advantages like these, you need to rely on an agent. Only an agent has the expertise needed to find the right asking price for your house. Here’s what’s at stake if that price isn’t accurate for today’s market value.

The price you set for your house sends a message to potential buyers.

Price it too low and you might raise questions about your home’s condition or lead buyers to assume something is wrong with it. Not to mention, if you undervalue your house, you could leave money on the table, which decreases your future buying power.

On the other hand, price it too high and you run the risk of deterring buyers from ever touring it in the first place. When that happens, you may have to do a price drop to try to re-ignite interest in your house when it sits on the market for a while. But be aware that a price drop can be seen as a red flag for some buyers who will wonder why the price was reduced and what that means about the home.

A recent article from NerdWallet sums it up like this:

“Your house’s market debut is your first chance to attract a buyer and it’s important to get the pricing right. If your home is overpriced, you run the risk of buyers not seeing the listing . . . But price your house too low and you could end up leaving some serious money on the table. A bargain-basement price could also turn some buyers away, as they may wonder if there are any underlying problems with the house.”

Think of pricing your home as a target. Your goal is to aim directly for the center – not too high, not too low, but right at market value.

Pricing your house fairly based on market conditions increases the chance you’ll have more buyers who are interested in purchasing it. That makes it more likely you’ll see multiple offers too. Plus, when homes are priced right, they still tend to sell quickly.

To get a high-level look into the potential downsides of over or underpricing your house and the perks that come with pricing it at market value, see the chart below:

Lean on a Professional’s Expertise to Price Your House Right

So why is an agent essential in finding the right price? Your local agent has the skill and the insight necessary to find the market value of your home. They’ll use their expertise to determine a realistic listing price by assessing:

- The prices of recently sold homes

- The current market conditions

- The size and condition of your house

- The location of your house

Bottom Line

Pricing your house at market value is critical, so don’t rely on guesswork. Let’s connect to make sure your house is priced right for today’s market.