Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Foreclosure Numbers Today Aren’t Like 2008

If you’ve been keeping up with the news lately, you’ve probably come across headlines talking about the increase in foreclosures in today’s housing market. This may have left you with some uncertainty, especially if you’re considering buying a home. It’s important to understand the context of these reports to know the truth about what’s happening today.

According to a recent report from ATTOM, a property data provider, foreclosure filings are up 2% compared to the previous quarter and 8% since one year ago. While media headlines are drawing attention to this increase, reporting on just the number could actually generate worry for fear that prices could crash. The reality is while increasing, the data shows a foreclosure crisis is not where the market is headed.

Let’s look at the latest information with context so we can see how this compares to previous years.

It Isn’t the Dramatic Increase Headlines Would Have You Believe

In recent years, the number of foreclosures has been down to record lows. That’s because, in 2020 and 2021, the forbearance program and other relief options for homeowners helped millions of homeowners stay in their homes, allowing them to get back on their feet during a very challenging period. And with home values rising at the same time, many homeowners who may have found themselves facing foreclosure under other circumstances were able to leverage their equity and sell their houses rather than face foreclosure. Moving forward, equity will continue to be a factor that can help keep people from going into foreclosure.

As the government’s moratorium came to an end, there was an expected rise in foreclosures. But just because foreclosures are up doesn’t mean the housing market is in trouble. As Clare Trapasso, Executive News Editor at Realtor.com, says:

“Many of these foreclosures would have occurred during the pandemic, but were put off due to federal, state, and local foreclosure moratoriums designed to keep people in their homes . . . Real estate experts have stressed that this isn’t a repeat of the Great Recession. It’s not that scores of homeowners suddenly can’t afford their mortgage payments. Rather, many lenders are now catching up. The foreclosures would have happened during the pandemic if moratoriums hadn’t halted the proceedings.”

In a recent article, Bankrate also explains:

“In the years after the housing crash, millions of foreclosures flooded the housing market, depressing prices. That’s not the case now. Most homeowners have a comfortable equity cushion in their homes. Lenders weren’t filing default notices during the height of the pandemic, pushing foreclosures to record lows in 2020. And while there has been a slight uptick in foreclosures since then, it’s nothing like it was.”

Basically, there’s not a sudden flood of foreclosures coming. Instead, some of the increase is due to the delayed activity explained above while more is from economic conditions.

To further paint the picture of just how different the situation is now compared to the housing crash, take a look at the graph below. It uses data on foreclosure filings for the first half of each year since 2008 to show foreclosure activity has been consistently lower since the crash.

While foreclosures are climbing, it’s clear foreclosure activity now is nothing like it was back then. Today, foreclosures are far below the record-high number that was reported when the housing market crashed.

While foreclosures are climbing, it’s clear foreclosure activity now is nothing like it was back then. Today, foreclosures are far below the record-high number that was reported when the housing market crashed.

In addition to all the factors mentioned above, that’s also largely because buyers today are more qualified and less likely to default on their loans.

Bottom Line

Right now, putting the data into context is more important than ever. While the housing market is experiencing an expected rise in foreclosures, it’s nowhere near the crisis levels seen when the housing bubble burst and that won’t lead to a crash in home prices.

Oops! Home Prices Didn’t Crash After All

During the fourth quarter of last year, many housing experts predicted home prices were going to crash this year. Here are a few of those forecasts:

Jeremy Siegel, Russell E. Palmer Professor Emeritus of Finance at the Wharton School of Business:

“I expect housing prices fall 10% to 15%, and the housing prices are accelerating on the downside.”

Mark Zandi, Chief Economist at Moody’s Analytics:

“Buckle in. Assuming rates remain near their current 6.5% and the economy skirts recession, then national house prices will fall almost 10% peak-to-trough. Most of those declines will happen sooner rather than later. And house prices will fall 20% if there is a typical recession.”

“Housing is already cooling in the U.S., according to July data that was reported last week. As interest rates climb steadily higher, Goldman Sachs Research’s G-10 home price model suggests home prices will decline by around 5% to 10% from the peak in the U.S. . . . Economists at Goldman Sachs Research say there are risks that housing markets could decline more than their model suggests.”

The Bad News: It Rattled Consumer Confidence

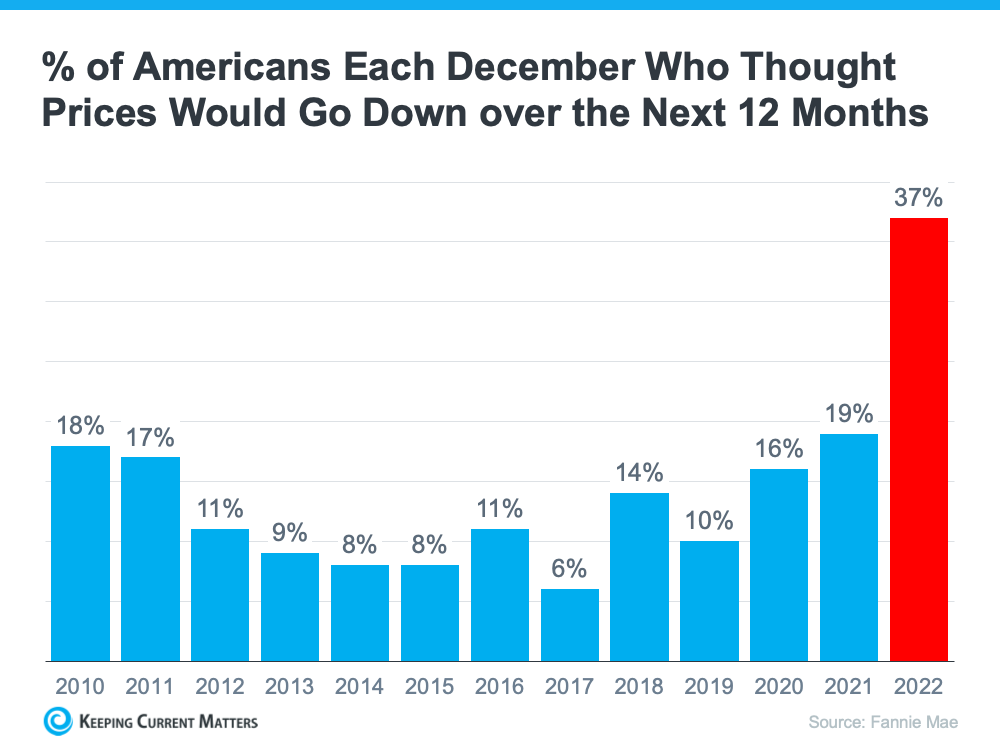

These forecasts put doubt in the minds of many consumers about the strength of the residential real estate market. Evidence of this can be seen in the December Consumer Confidence Survey from Fannie Mae. It showed a larger percentage of Americans believed home prices would fall over the next 12 months than in any other December in the history of the survey (see graph below). That caused people to hesitate about their homebuying or selling plans as we entered the new year.

The Good News: Home Prices Never Crashed

However, home prices didn’t come crashing down and seem to be already rebounding from the minimal depreciation experienced over the last several months.

In a report just released, Goldman Sachs explained:

“The global housing market seems to be stabilizing faster than expected despite months of rising mortgage rates, according to Goldman Sachs Research. House prices are defying expectations and are rising in major economies such as the U.S.,. . . ”

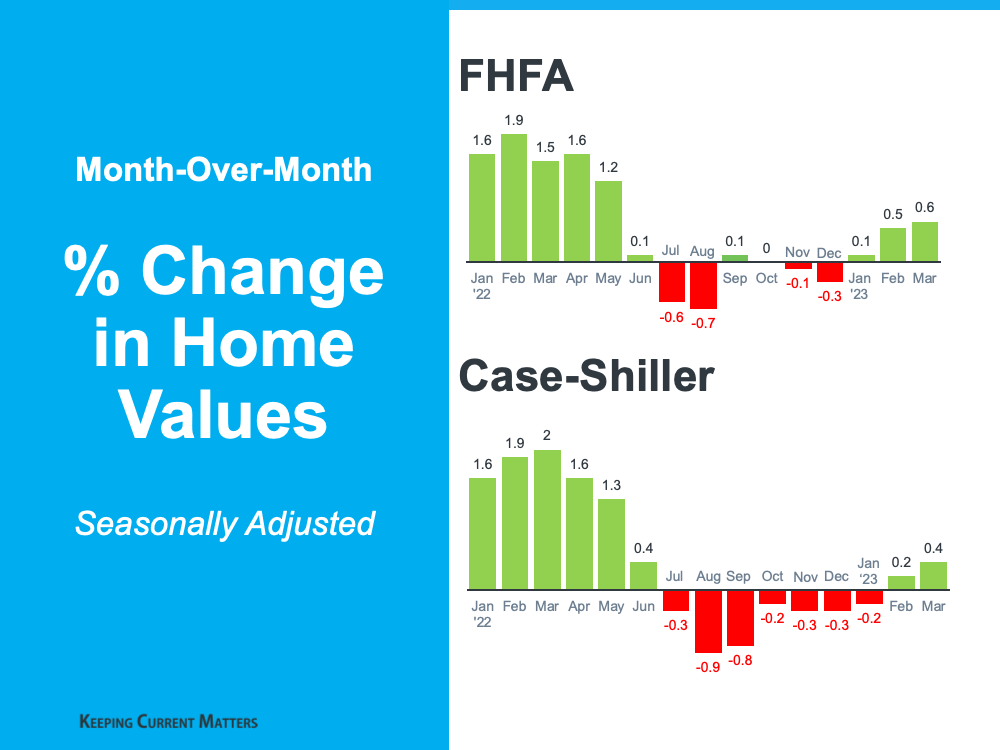

Those claims from Goldman Sachs were verified by the release last week of two indexes on home prices: Case-Shiller and the FHFA. Here are the numbers each reported:

Home values seem to have turned the corner and are headed back up.

Bottom Line

The housing market is much stronger than many think. To get a true evaluation of your local market, reach out to a trusted real estate professional.

Keys to Success for First-Time Homebuyers

Buying your first home is an exciting decision and a major milestone that has the power to change your life for the better. As a first-time homebuyer, it’s a vision you can bring to life, but, as the National Association of Realtors (NAR) shares, you’ll have to overcome some factors that have made it more challenging in recent years:

“Since 2011, the share of first-time home buyers has been under the historical norm of 40% as buyers face tight inventory, rising home prices, rising rents, and high student debt loads.”

That said, if you’re looking to purchase your first home, here are two things you can consider to help make your dreams a reality.

Save Money with First-Time Homebuyer Programs

Being able to pay for the initial costs and fees associated with homeownership can feel like a major hurdle. Whether that’s getting a loan, being able to put together a down payment, or having money for closing costs – there are a variety of expenses that can make buying your first home feel challenging.

Fortunately, there are a lot of public and private first-time homebuyer programs that can help you get a loan with little-to-no money upfront. CNET explains:

“A first-time homebuyer program can help make homeownership more affordable and accessible by offering lower mortgage rates, down payment assistance, and tax incentives.”

In fact, as Bankrate says, many of these programs are offered by state and local governments:

“Many states and local governments have programs that offer down payment or closing cost assistance – either low-interest-rate loans, deferred loans or even forgivable loans (aka grants) – to people looking to buy their first house . . .”

To take advantage of these programs, contact the housing authority in your state and browse sites like Down Payment Resource.

The Supply of Homes for Sale Is Low, So Explore Every Possibility

It’s a sellers’ market, meaning there aren’t enough homes on the market to meet buyer demand. So, how can you be sure you’re doing everything you can to find a home that works for you? You can increase your options by considering condominiums (condos) and townhomes. U.S. News tells us these housing types are often less expensive than single-family homes:

“Condos are usually less expensive than standalone houses . . . They are also less expensive to insure.”

One reason why they may be more affordable is because they’re often smaller. But they still give you the chance to get your foot in the door and achieve your dream of owning and building equity. Beyond that, another major perk is they typically require less maintenance. As U.S. News says in the same article:

“The strongest reason for purchasing a condo is that all external maintenance is usually covered by the condo association, such as landscaping, pool maintenance, external painting, paving, plowing and more. This fee also covers some internal maintenance, such as gas, electric, plumbing, HVAC and other mechanical systems.”

Townhomes and condos are great ways to get into homeownership. Owning your home allows you to build equity, increase your net worth, and can fuel a future move.

The best way to make sure you’re set up for success, especially if you’re just starting out, is to work with a trusted real estate agent. They can educate you on the homebuying process, help you understand your local area to find options that are right for you, and coach you through making an offer in a competitive market.

Bottom Line

Today’s housing market provides some challenges for first-time homebuyers. But, there are still ways to achieve your goals, like utilizing first-time homebuyer programs and considering all of your housing options. Connect with a local real estate professional so you have an expert on your side who can help you navigate the process.

The Benefits of Selling Now, According to Experts

If you’re trying to decide if now’s the time to sell your house, here’s what you should know. The limited number of homes available right now gives you a big advantage. That’s because there are more buyers out there than there are homes for sale. And, with so few homes on the market, buyers will have fewer options, so you set yourself up to get the most eyes possible on your house.

Here’s what industry experts are saying about why selling now has its benefits:

Lawrence Yun, Chief Economist at the National Association of Realtors (NAR):

“Inventory levels are still at historic lows. Consequently, multiple offers are returning on a good number of properties.”

Selma Hepp, Chief Economist at CoreLogic:

“We have not seen the traditional uptick in new listings from existing homeowners, so undersupply of housing will continue to heighten market competition and put pressure on prices in most regions. Some markets are already heating up considerably, but price premiums that we saw last spring and summer are unlikely.”

Clare Trapasso, Executive News Editor at Realtor.com:

“Well-priced, move-in ready homes with curb appeal in desirable areas are still receiving multiple offers and selling for over the asking price in many parts of the country . . .”

Jeff Tucker, Senior Economist at Zillow:

“. . . sellers who price and market their home competitively shouldn’t have a problem finding a buyer.”

Bottom Line

If you’re thinking about selling your house, connect with a real estate advisor who can share the expert insights you need to make the best possible move today.

Owning a Home Helps Protect Against Inflation

You’re probably feeling the impact of high inflation every day as prices have gone up on groceries, gas, and more. If you’re a renter, you’re likely experiencing it a lot as your rent continues to rise. Between all of those elevated costs and uncertainty about a potential recession, you may be wondering if it still makes sense to buy a home today. The short answer is – it does. Here’s why.

Homeownership actually shields you from the rising costs inflation brings.

Freddie Mac explains how:

“Not only will buying today help you begin to build equity, a fixed-rate mortgage can stabilize your monthly housing costs for the long-term even while other life expenses continue to rise – as has been the case the past few years.”

Unlike rents, which tend to rise with time, a fixed-rate mortgage payment is predictable over the life of the mortgage (typically 15 to 30 years). And, when the cost of most everything else is rising, keeping your housing payment stable is especially important.

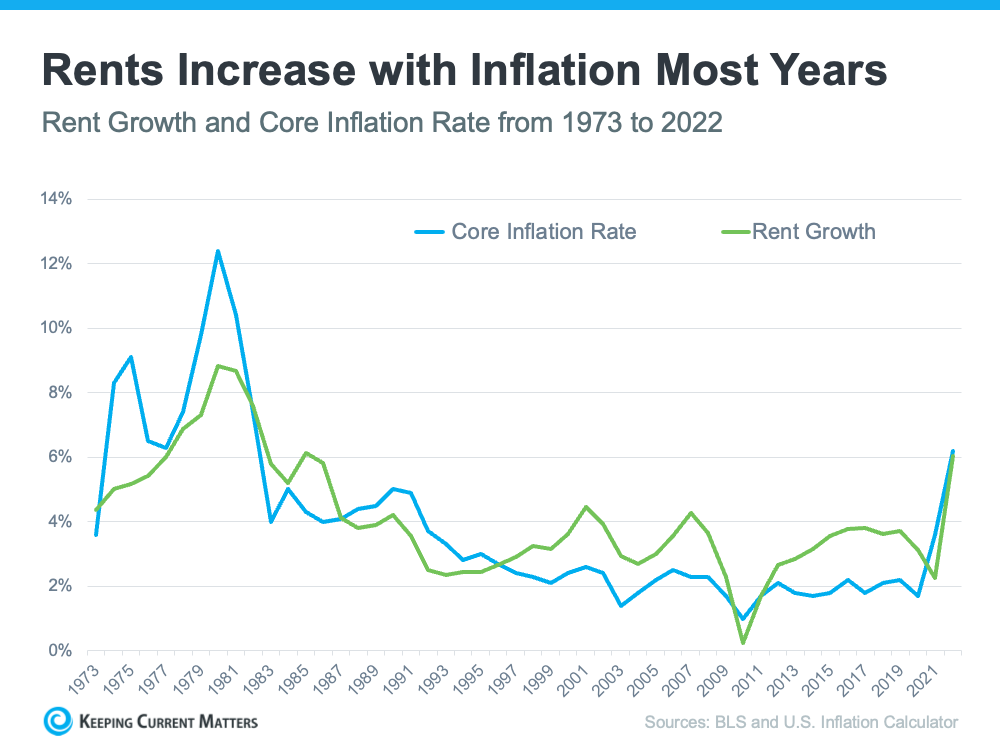

The alternative to homeownership is renting – and rents tend to move alongside inflation. That means as inflation goes up, your monthly rent payments tend to go up, too (see graph below):

A fixed-rate mortgage allows you to protect yourself from future rent hikes. With inflation still high, when your rental agreement comes up for renewal, your property manager may decide to increase your payments to offset the impact of inflation. Maybe that’s why, according to a recent survey, 73% of property managers plan to raise rents over the next two years.

Having your largest monthly expense remain stable in a time of economic uncertainty is a major perk of homeownership. If you continue to rent, you don’t have that same benefit and aren’t as protected from rising costs.

Bottom Line

A stable housing payment is especially important in times of high inflation. Connect with a real estate agent so you can learn more and start your journey to homeownership today.

Why Buyers Need an Expert Agent by Their Side

The process of buying a home can feel a bit intimidating, even under normal circumstances. But today’s market is still anything but normal. There continues to be a very limited number of homes for sale, and that’s creating bidding wars and driving home prices back up as buyers compete over the available homes.

Navigating all of this can be daunting if you’re trying to do it alone. That’s why having a skilled expert to guide you through the home-buying process is essential, especially today. Bankrate shares this perspective:

“Advice and guidance from a professional real estate agent can be invaluable, particularly amid a hot or unpredictable housing market.”

Here are just a few of the ways a real estate expert makes a big difference:

- Experience – Real estate professionals know the ins and outs of what’s happening today, how it impacts buyers, and how to navigate any hurdles that may pop up.

- Education – Knowledge is power when it comes to buying a home. Your advisor will simply and effectively explain market conditions and translate what they mean for you so you can feel confident in your decision.

- Negotiations – Your real estate advisor advocates for your best interests. Having an expert on your side provides assistance with the purchase agreement. An agent can also help you negotiate potential seller concessions if the inspection reveals issues with the home.

- Contracts – Real estate advisors guide you through the disclosures and contracts necessary in today’s heavily regulated environment.

- Pricing – Making an offer and negotiating with a seller can be one of the most difficult and stressful parts of the home-buying process. A skilled agent will help you understand what similar homes are selling for so you have the full picture of what you may want to offer.

All of these reasons combined may be why 86% of recent buyers used an agent according to the latest Home Buyers and Sellers Generational Trends Report from the National Association of Realtors (NAR). NAR also has this to say about why an agent is so essential today:

“A great real estate agent will guide you through the home search with an unbiased eye, helping you meet your buying objectives while staying within your budget. Agents are also a great source when you have questions about local amenities, utilities, zoning rules, contractors, and more.”

What’s the Key To Choosing the Right Expert?

It starts with trust. You’ll want to know you can trust the advice they’re giving you, so you need to make sure you’re connected with a true professional. No one can provide perfect advice because it’s impossible to know exactly what will happen at every turn – especially in today’s market. But a true professional can give you the best possible advice based on the information and situation at hand.

They’ll help advocate for you throughout the process and coach you on the essential knowledge you need to make confident decisions. That’s exactly what you want and deserve.

Bottom Line

It’s critical to have an expert on your side who is skilled in navigating today’s housing market. If you’re planning to buy a home this year, connect with a real estate advisor who will give you the best advice and guide you along the way.

Powerful Job Market Fuels Homebuyer Demand

The spring housing market has been surprisingly active this year. Even with affordability challenges and a limited number of homes for sale, buyer demand is strong and getting stronger.

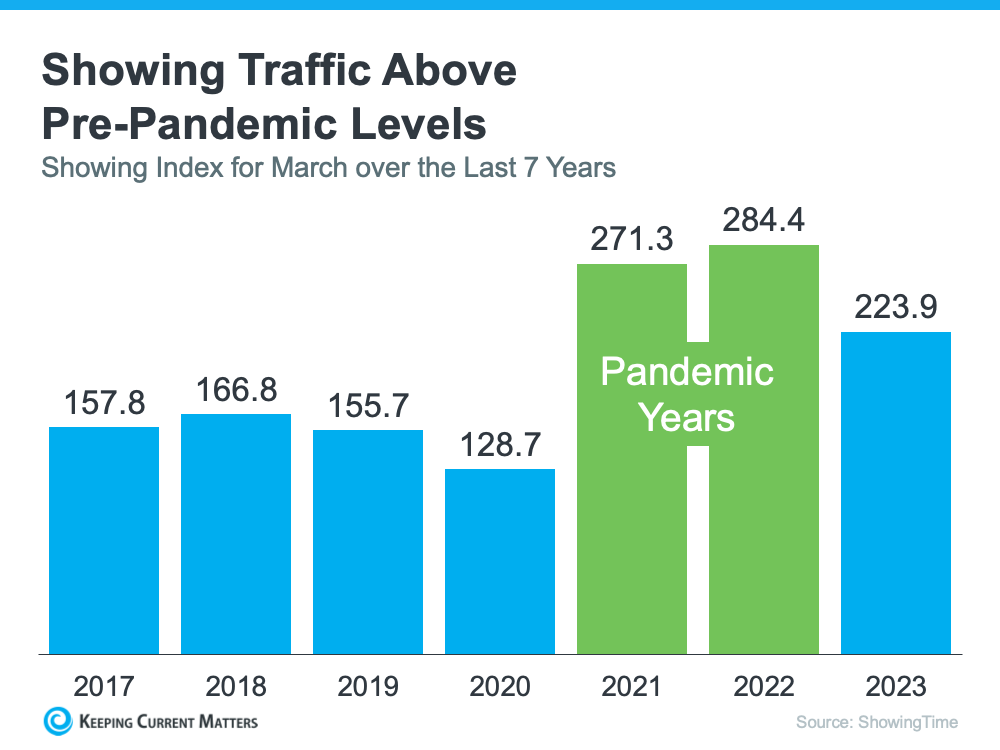

One way we know there are interested buyers right now is because showing traffic is up. Data from the latest ShowingTime Showing Index, which is a measure of buyers actively touring homes, makes it clear more people are out looking at homes than there were prior to the pandemic (see graph below):

And though there’s less traffic than the buyer frenzy of the past couple of years, we’re not far off that pace. There are a lot of interested buyers checking out available homes right now.

But why are buyers so active at a time when mortgage rates are higher than they were just last year?

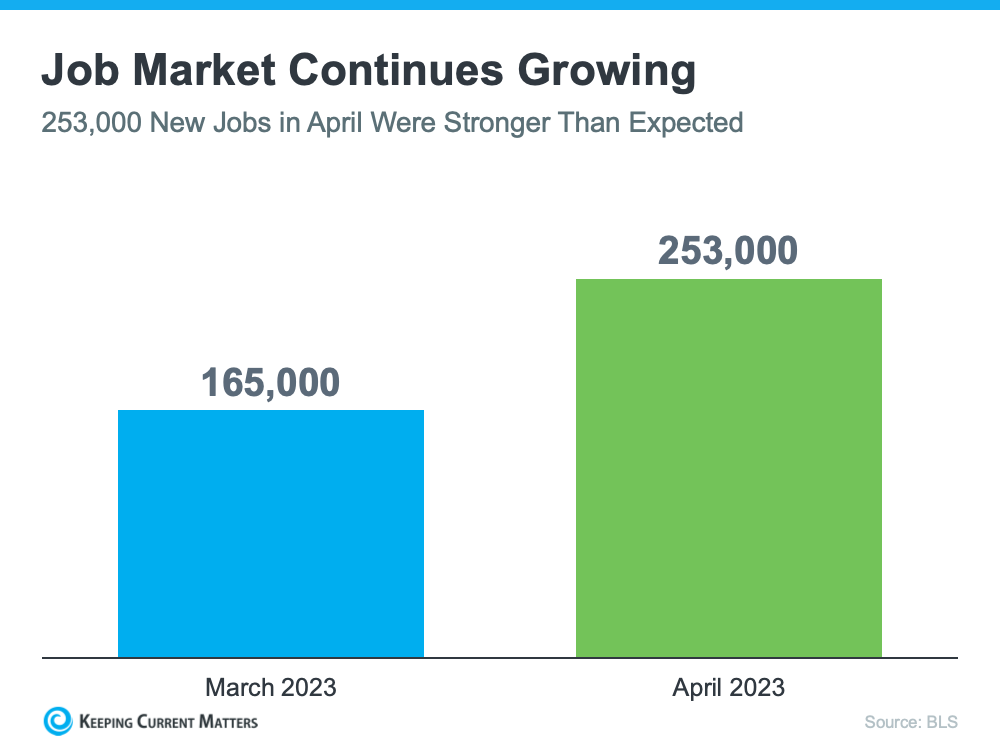

The Job Market Is Growing at a Stronger-Than-Expected Pace

With inflation still high, the Federal Reserve (the Fed) repeatedly hiking the Federal Funds Rate, and a lot of chatter in the media about a recession, it might surprise you just how strong today’s job market is. What might be even more surprising is the fact that it appears to be getting stronger (see graph below):

Each month, the Bureau of Labor Statistics (BLS) reports how many new jobs were added to the U.S. job market. The graph above shows 88,000 more jobs were created in April than in March. In fact, the April numbers beat expert projections. That’s a solid indicator the job market is growing.

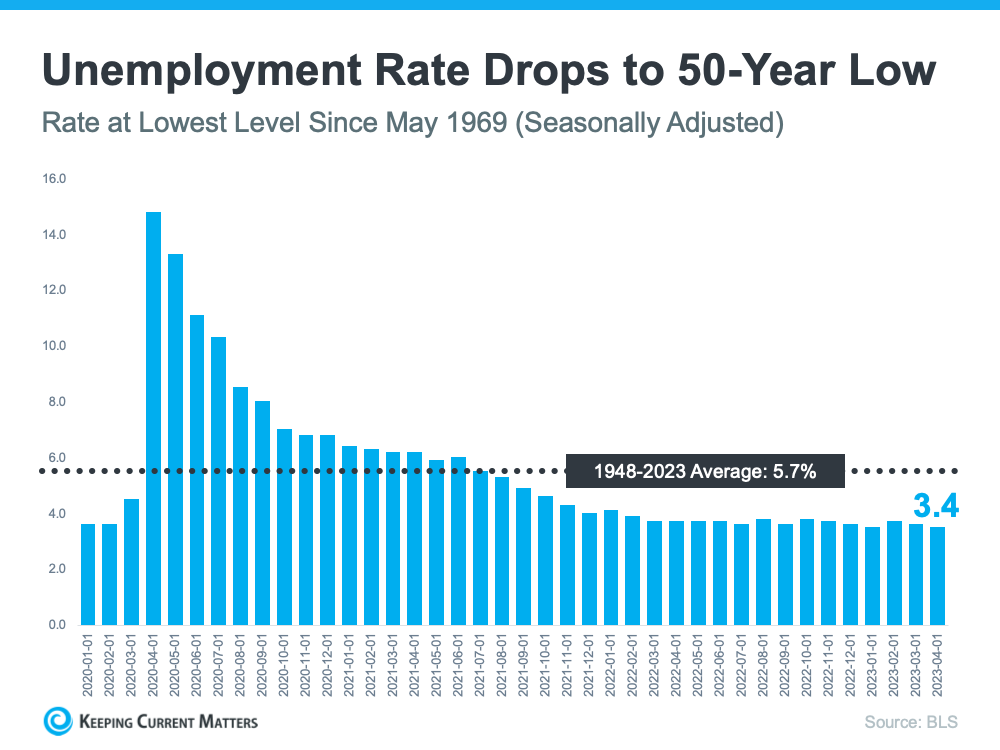

Unemployment Is at a Near All-Time Low

Ever since the Fed began fighting inflation, many people expected the low unemployment rate we’ve seen over the past couple of years to rise – but that hasn’t happened.

In fact, what has happened is the unemployment rate has dropped to 3.4% – a 50-year low (see graph below):

With so many people steadily employed and financially stable right now, they’re still able to seriously consider buying a home.

What This Means for You

If you’re thinking about selling your house this year, a market with active buyers is music to your ears. That’s because there’ll be increased interest in your home when you put it on the market, especially at a time when the number of homes for sale is so low.

To get started, your best resource is an experienced real estate agent. They can help you price your house appropriately, navigate the offers you’ll receive, negotiate effectively, and minimize your stress and hassle.

Bottom Line

There are plenty of buyers out there right now trying to find a home that fits their needs. That’s because the job market is strong, and many people have the stable income needed to seriously consider homeownership. To put your house on the market and get in on the action, reach out to a trusted real estate agent.

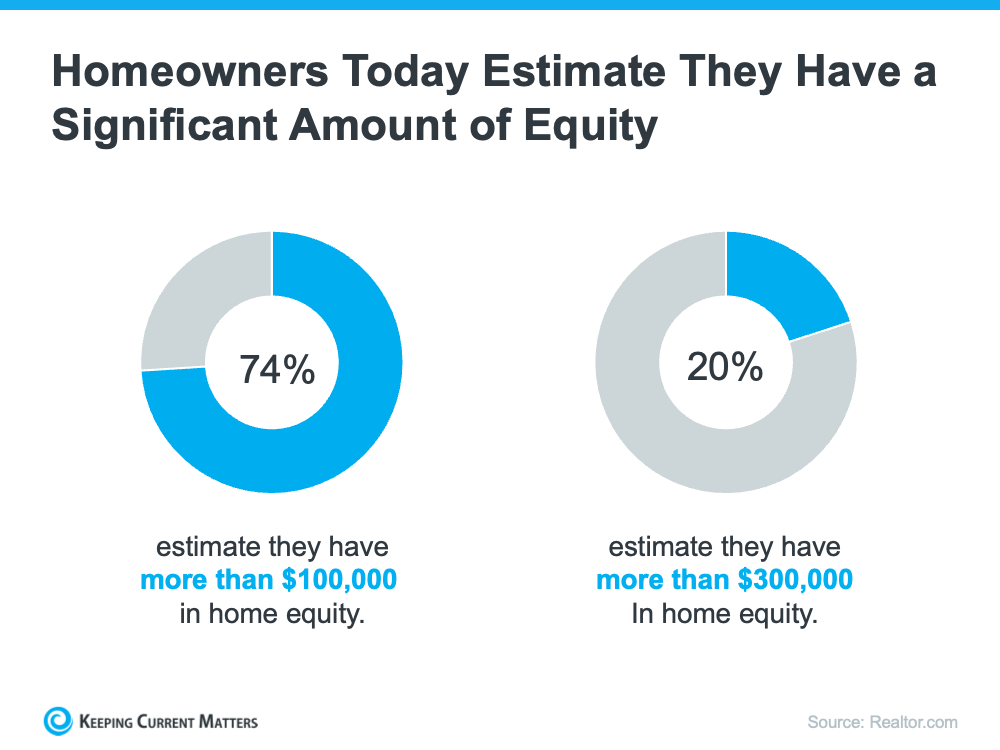

Homeowners Have Incredible Equity To Leverage Right Now

Even though home prices have moderated over the last year, many homeowners still have an incredible amount of equity. But what is equity? In the simplest terms, equity is the difference between the market value of your home and the amount you owe on your mortgage. The National Association of Realtors (NAR) explains how your equity grows over time:

“Housing wealth (home equity or net worth) gains are built up through price appreciation and by paying off the mortgage.”

How Your Equity Can Help You Achieve Your Goals

The equity you build up over the years can be used to your advantage when you sell your current house and buy your next home. If you no longer have the space you need, it might be time to move into a larger home. Or it’s possible you have too much space and need something smaller. No matter the situation, your equity can be a powerful tool you can use to help you make a move in today’s market. That’s because it may be some (if not all) of what you need for your down payment on your next home.

And how much equity you have may surprise you. A recent survey from Realtor.com finds many homeowners today estimate they’ve built up a significant amount of equity:

The latest data from CoreLogic helps solidify why homeowners are feeling so good about the equity they’ve likely gained over time. As Selma Hepp, Chief Economist for CoreLogic, says:

“While equity gains contracted in late 2022 due to home price declines in some regions, U.S. homeowners on average still have about $270,000 in equity, nearly $90,000 more than they had at the onset of the pandemic.”

How a Skilled Real Estate Agent Can Help

If you’re looking to leverage your equity to boost your buying power in today’s market, having a trusted agent by your side makes a difference.

A real estate professional can help you better understand the value of your home, so you’ll get a clearer picture of how much equity you likely have. As a recent article from Bankrate says:

“Hiring a skilled real estate agent can give you a realistic estimate of home prices in your area and how to price your current home. Using that figure, you can calculate how much equity you have and what your net proceeds will look like, so you can apply that money toward the down payment and closing costs of your new home.”

Having a solid understanding of your equity is key when it comes to making decisions about buying or selling your home. A skilled agent can help you navigate the often-complicated process of selling your house and ensure the transaction goes smoothly.

Bottom Line

Today, many homeowners are sitting on a substantial amount of equity, and you may be one of them. A real estate agent can help you estimate how much equity you have and plan how you can use it toward the purchase of your next home.

The Best Time To Sell Your House Is When Others Aren’t Selling

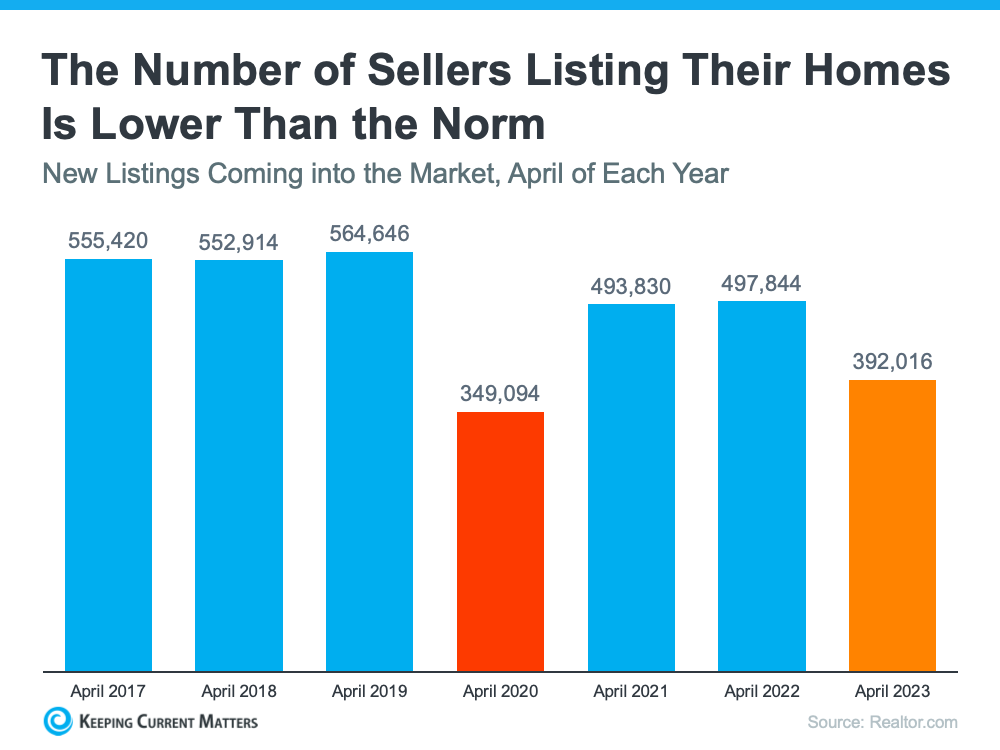

If you’re thinking about selling your house, you should know the number of homes for sale right now is low. That’s because, this season, fewer sellers are listing their houses for sale than the norm.

Looking back at every April since 2017, the only year when fewer sellers listed their homes was in April 2020, when the pandemic hit and stalled the housing market (shown in red in the graph below). In more typical years, roughly 500,000 sellers add their homes to the market in April. This year, we saw fewer than 400,000 sellers entering the market in April (see graph below):

While there are several factors contributing to this trend, one thing keeping inventory low right now is that some homeowners are reluctant to move when the mortgage rate they have on their current house is lower than the one they could get today on their next house. It’s called a rate lock.

As a recent survey from Realtor.com explains, 56% of people who are planning to sell in the next 12 months say they’re waiting for rates to come down.

While this wait-and-see approach is right for some sellers, it also creates an opening for more eager sellers to jump in now.

If your current house truly doesn’t fit your needs anymore and you’re ready to move, don’t miss this chance to stand out. When fewer sellers put their homes up for sale, buyers will have fewer options, so you set yourself up to get the most eyes on your house. That’s why your house could see multiple offers as buyers compete over the limited supply of homes for sale – especially if you price it right.

As Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), says:

“Inventory levels are still at historic lows . . . Consequently, multiple offers are returning on a good number of properties.”

Bottom Line

If you’re ready to sell now, beat the competition before it comes onto the market. If you do, your house should stand out and could get multiple offers—partner with a real estate professional to get your home on the market.

It May Be Time To Consider a Newly Built Home

If you’re looking to buy a house, you may find today’s limited supply of homes available for sale challenging. When housing inventory is as low as it is right now, it can feel like a bit of an uphill battle to find the perfect home for you because there just isn’t that much to choose from. If you need to open up your pool of options, it may be time to consider a newly built home.

According to the latest data from the U.S. Census, there’s positive news when it comes to new home construction. When you look at the first three months of this year, you’ll find:

- More new homes were completed and are ready to sell. This gives you more move-in-ready options for your search.

- Builders broke ground and started construction on more single-family homes. This means there are more homes intended for one household in the beginning stages of construction, allowing you the opportunity to customize one to your liking.

- The number of permits for building new single-family homes ticked up. This shows builders are ramping up to start on even more home construction soon.

And, while this is all good news for broadening your options for your home search, there are other perks that come with considering a newly built home.

Customization

When you buy a new home under construction, you can tailor it to your unique needs and taste. Bankrate says:

“Building means customizing. . . . instead of wishing your home had a certain kind of flooring, a sunroom or some other special amenity, you’ll be able to tailor the property to your exact needs.”

Brand New Everything

Another perk of a new home is that nothing in the house is used. It’s all brand new and uniquely yours from day one.

Minimal Repairs

And, because everything is new, you’ll likely find there are fewer maintenance and repair needs upfront. As Realtor.com explains:

“. . . if something does go wrong with your new home, not only are there likely some manufacturer warranties in place, but many builders also include additional home warranties . . .”

Energy Efficiency

Lastly, building a home gives you the opportunity to incorporate more energy-efficient options that can help lower your costs over time – which can feel especially important when inflation’s raising many of the costs around you.

Bottom Line

If you’re having trouble finding your dream home in today’s market, it may be time to consider newly built homes as an option. Partner with a real estate professional to learn more about what’s available in your local area.