Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

What Experts Are Saying About the 2023 Housing Market

If you’re thinking about buying or selling a home soon, you probably want to know what you can expect from the housing market this year. In 2022, the market underwent a major shift as economic uncertainty and higher mortgage rates reduced buyer demand, slowed the pace of home sales, and moderated home prices. But what about 2023?

An article from HousingWire offers this perspective:

“The red-hot housing market of the past 2 ½ years was characterized by sub-three percent mortgage rates, fast-paced bidding wars and record-low inventory. But more recently, market conditions have done an about-face. . . . now is the opportunity for everyone to become re-educated about what a ‘typical’ housing market looks like.”

This year, experts agree we may see the return of greater stability and predictability in the housing market if inflation continues to ease and mortgage rates stabilize. Here’s what they have to say.

The 2023 forecast from the National Association of Realtors (NAR) says:

“While 2022 may be remembered as a year of housing volatility, 2023 likely will become a year of long-lost normalcy returning to the market, . . . mortgage rates are expected to stabilize while home sales and prices moderate after recent highs, . . .”

Danielle Hale, Chief Economist at realtor.com, adds:

“. . . buyers will not face the extreme competition that was commonplace over the past few years.”

Lawrence Yun, Chief Economist at NAR, explains home prices will vary by local area, but will net neutral nationwide as the market continues to adjust:

“After a big boom over the past two years, there will essentially be no change nationally . . . Half of the country may experience small price gains, while the other half may see slight price declines.”

Mark Fleming, Chief Economist at First American, says:

“The housing market, once adjusted to the new normal of higher mortgage rates, will benefit from continued strong demographic-driven demand relative to an overall, long-run shortage of supply.”

Bottom Line

If you’re looking to buy or sell a home this year, the best way to ensure you’re up to date on the latest market insights is to partner with a trusted real estate advisor. Let’s connect.

3 Best Practices for Selling Your House This Year

A new year brings with it the opportunity for new experiences. If that resonates with you because you’re considering making a move, you’re likely juggling a mix of excitement over your next home and a sense of attachment to your current one.

A great way to ease some of those emotions and ensure you’re feeling confident in your decision is to keep these three best practices in mind.

1. Price Your Home Right

The housing market shifted in 2022 as mortgage rates rose, buyer demand eased, and the number of homes for sale grew. As a seller, you’ll want to recognize things are different now and price your house appropriately based on where the market is today. Greg McBride, Chief Financial Analyst at Bankrate, explains:

“Price your home realistically. This isn’t the housing market of April or May, so buyer traffic will be substantially slower, but appropriately priced homes are still selling quickly.”

If you price your house too high, you run the risk of deterring buyers. And if you go too low, you’re leaving money on the table. An experienced real estate agent can help determine what your ideal asking price should be.

2. Keep Your Emotions in Check

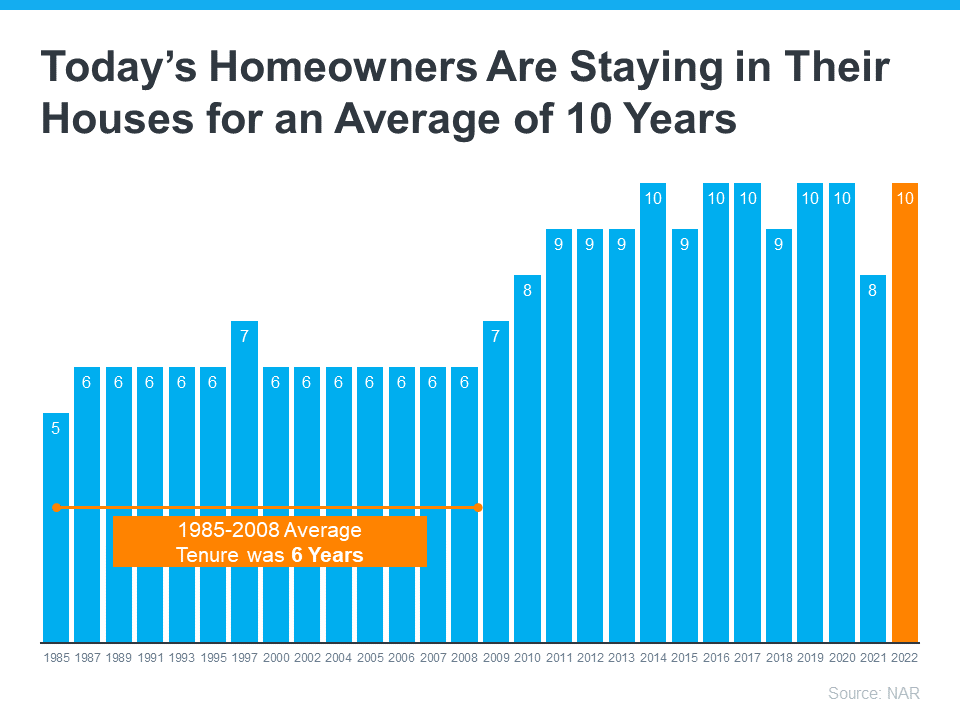

Today, homeowners are living in their houses longer. According to the National Association of Realtors (NAR), since 1985, the average time a homeowner has owned their home has increased from 5 to 10 years (see graph below):

This is several years longer than what used to be the historical norm. The side effect, however, is when you stay in one place for so long, you may get even more emotionally attached to your space. If it’s the first home you bought or the house where your loved ones grew up, it very likely means something extra special to you. Every room has memories, and it’s hard to detach from the sentimental value.

For some homeowners, that makes it even harder to negotiate and separate the emotional value of the house from fair market price. That’s why you need a real estate professional to help you with the negotiations along the way.

3. Stage Your Home Properly

While you may love your decor and how you’ve customized your home over the years, not all buyers will feel the same way about your design. That’s why it’s so important to make sure you focus on your home’s first impression so it appeals to as many buyers as possible. As NAR says:

“Staging is the art of preparing a home to appeal to the greatest number of potential buyers in your market. The right arrangements can move you into a higher price-point and help buyers fall in love the moment they walk through the door.”

Buyers want to envision themselves in the space so it truly feels like it could be their own. They need to see themselves inside with their furniture and keepsakes – not your pictures and decorations. A real estate professional can help you with tips to get your house ready to sell.

Bottom Line

If you’re considering selling your house, let’s connect so you have the help you need to navigate through the process while prioritizing these best practices.

Confused About What’s Going on in the Housing Market? Lean on a Professional.

Confused About What’s Going on in the Housing Market? Lean on a Professional.

If you’re thinking about buying or selling a home, you probably want to know what’s really happening with home prices, mortgage rates, housing supply, and more. That’s not an easy task considering how sensationalized headlines are today. Jay Thompson, Real Estate Industry Consultant, explains:

“Housing market headlines are everywhere. Many are quite sensational, ending with exclamation points or predicting impending doom for the industry. Clickbait, the sensationalizing of headlines and content, has been an issue since the dawn of the internet, and housing news is not immune to it.”

Unfortunately, when information in the media isn’t clear, it can generate a lot of fear and uncertainty in the market. As Jason Lewris, Cofounder and Chief Data Officer at Parcl, says:

“In the absence of trustworthy, up-to-date information, real estate decisions are increasingly being driven by fear, uncertainty, and doubt.”

But it doesn’t have to be that way. Buying or selling a home is a big decision, and it should be one you feel confident making. To help you separate fact from fiction and get the answers you need, lean on a local real estate advisor.

A trusted expert is your best resource to understand what’s happening at the national and local levels. They’ll be able to debunk the headlines using data you can trust. And using their in-depth knowledge of the industry, they’ll provide context so you know how current trends compare to the normal ebbs and flows in the industry, historical data and more.

Then, to make sure you have the full picture, they’ll tell you if your local area is following the national trend or if they’re seeing something different in your market. Together, you’ll use all of that information to make the best possible decision for you.

After all, making a move is a potentially life-changing milestone. It should be something you feel ready for and excited about. And that’s where an agent comes in.

Bottom Line

If you have questions about the headlines or what’s happening in the housing market today, let’s connect so you have expert insights and advice on your side.

Thank You for All of Your Support

Thank You for All of Your Support

What Makes a House a Home?

What Makes a House a Home?

There’s no denying the long-term financial benefits of owning a home, but today’s housing market may have you wondering if now’s still the time to buy. While the financial aspects of buying a home are important, the non-financial and emotional reasons are too.

Home means something different to all of us. Whether it’s sharing memories with loved ones at the kitchen table or settling in to read a book in a favorite chair, the emotional connections to our homes can be just as important as the financial ones. Here are some of the things that make a house a home.

1. You Can Be Proud of Your Accomplishment

Buying a home is a major life milestone. Whether you’re setting out to buy your first home or your fifth, congratulations will be in order when you’ve achieved your goal. The sense of accomplishment you’ll feel at the end of your journey will truly make your home feel like a special place.

2. You Have Your Own Designated Happy Place

Owning your own home offers not only safety and security, but also a comfortable place where you can relax and unwind after a long day. Sometimes that’s just what you need to feel recharged and content.

3. You Can Find the Space To Meet Your Needs

Whether you want more room for your changing lifestyle (like retirement, dedicated space for a hobby, or a personal gym) or you simply prefer to have a large backyard for entertaining, you can invest in a home that truly works for your evolving needs.

4. You Can Customize Your Surroundings

Looking to try one of those decorative wall treatments you saw online? Tired of paying an additional pet deposit for your apartment building? Or maybe you want to create an in-home yoga studio. You can do all these things in your own home.

Bottom Line

Whether you’re planning to purchase your first home or you’re ready to buy a different home to meet your needs, consider the emotional benefits that can turn a house into a happy home. When you’re ready to make a move, let’s connect.

Homeowners Still Have Positive Equity Gains over the Past 12 Months

If you’re a homeowner, your net worth got a big boost over the past few years thanks to rapidly rising home prices. Here’s how it happened and what it means for you, even as the market moderates.

Equity is the current value of your home minus what you owe on the loan.

Because there was a significant imbalance between the number of homes available for sale and the number of buyers looking to make a purchase over the past few years, home prices appreciated substantially.

And while home price appreciation has moderated this year, and even depreciated slightly in some overheated markets, that doesn’t mean you’ve lost all the equity you gained during the pandemic frenzy.

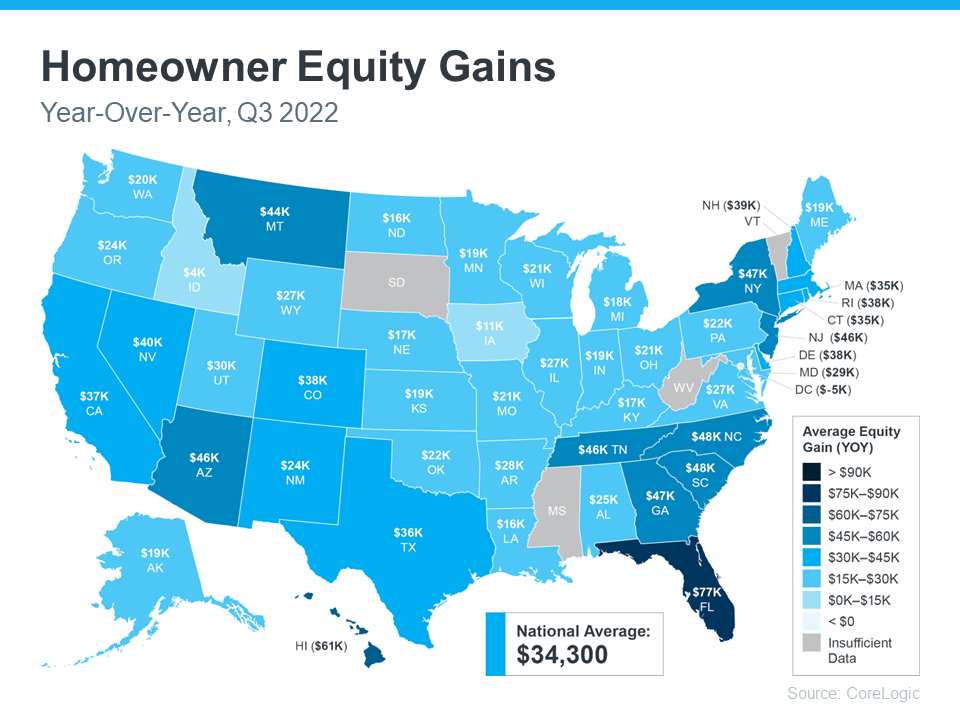

To prove you still have equity you can use, the latest Homeowner Equity Insights from CoreLogic finds the average homeowner equity has actually grown by $34,300 over the past 12 months.

That’s right, despite the headlines, the average homeowner still gained positive equity over the last year in just about every market. While the gains aren’t as dramatic as they were in the previous quarter due to home price moderation, they’re still significant. And if you’ve been in your home for longer than a year, chances are you have even more equity than you realize.

While that’s the national number, if you want to know what happened over the past year in your area, look at the map below from CoreLogic:

Why This Is So Important Right Now

While equity helps increase your overall net worth, it can also help you achieve other goals, like buying your next home. When you sell your current house, the equity you’ve built up comes back to you in the sale, and it may be just what you need to cover a large portion – if not all – of the down payment on your next home.

So, if you’ve been holding off on selling because you weren’t sure what the headlines meant for your bottom line, rest assured you’ve still gained equity in recent years, and it can help fuel your move.

Bottom Line

If you’re planning to make a move, the equity you’ve gained over time can make a big impact. To find out just how much equity you have in your current home and how you can use it to fuel your next purchase, let’s connect.

Planning to Retire? It Could Be Time To Make a Move.

Planning to Retire? It Could Be Time To Make a Move.

If you’re thinking about retirement or have already retired this year, you may be planning your next steps. One of your goals could be selling your house and finding a home that more closely fits your needs.

Fortunately, you may be in a better position to make a move than you realize. Here are a few things to think about when making that decision.

Consider How Long You’ve Been in Your Home

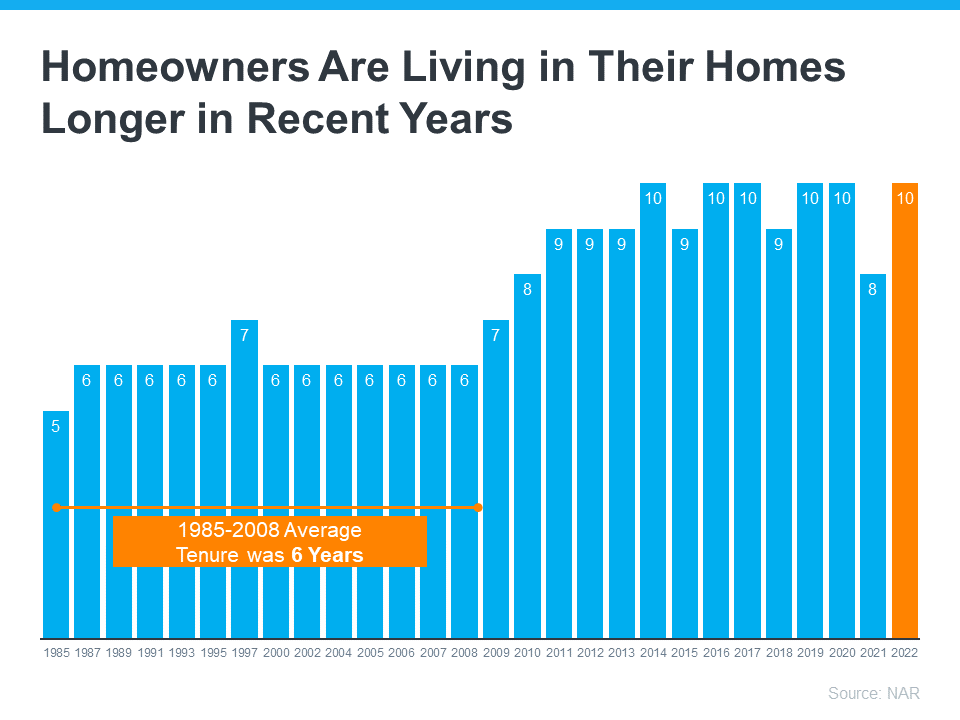

From 1985 to 2008, the average length of time homeowners typically stayed in their homes was only six years. But according to the National Association of Realtors (NAR), that number is rising today, meaning many homeowners are living in their houses even longer (see graph below):

When you live in a home for a significant period of time, it’s natural for you to experience a number of changes in your life while you’re in that house. As those life changes and milestones happen, your needs may change. And if your current home no longer meets them, you may have better options waiting for you.

Consider the Equity You’ve Gained

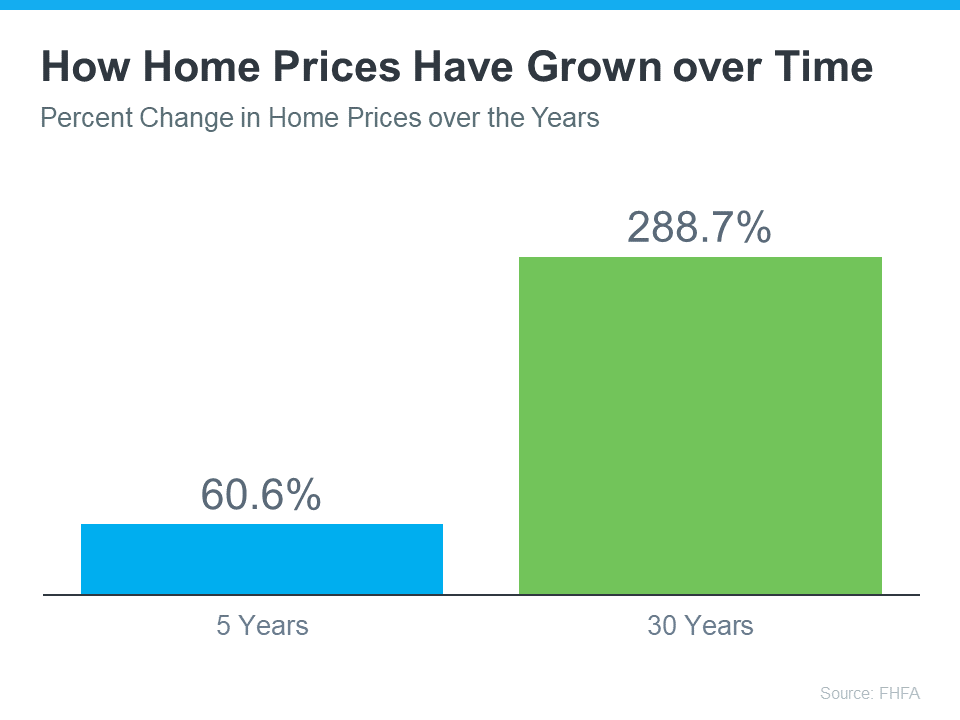

Additionally, if you’ve been in your home for more than a few years, you’ve likely built up significant equity that can fuel your next move. That’s because the longer you’ve been in your home, the more likely it’s grown in value due to home price appreciation. Data from the Federal Housing Finance Agency (FHFA) illustrates that point (see graph below):

While home price growth varies by state and local area, the national average shows the typical homeowner who’s been in their house for five years saw it increase in value by over 50%. And the average homeowner who’s owned their home for 30 years saw it almost triple in value over that time.

Consider Your Retirement Goals

Whether you’re looking to downsize, relocate to a dream destination, or move so you live closer to loved ones, that equity can help you achieve your homeownership goals. NAR shares that for recent home sellers, the primary reason to move was to be closer to loved ones. Plus, retirement played a large role for those moving greater distances.

Whatever your home goals are, a trusted real estate advisor can work with you to find the best option. They’ll help you sell your current house and guide you as you buy the home that’s right for you and your lifestyle today.

Bottom Line

Retirement can bring about major changes in your life, including what you need from your home. Let’s connect to explore your opportunities in our local market.

You May Have More Negotiation Power When You Buy a Home Today

Did the frequency and intensity of bidding wars over the past two years make you put your home search on hold? If so, you should know the hyper competitive market has cooled this year as buyer demand has moderated and housing supply has grown. Those two factors combined mean you may see less competition from other buyers.

And with less competition comes more opportunity. Here are two trends that may be the news you need to reenter the market.

1. The Return of Contingencies

Over the last two years, more buyers were willing to skip important steps in the homebuying process, like the appraisal or the inspection, in hopes of gaining an advantage in a bidding war. But now, things are different.

The latest data from the National Association of Realtors (NAR) shows the percentage of buyers waiving their home inspection or appraisal is down. And a recent article from realtor.com points out more sellers are accepting contingencies:

“A year ago, sellers were calling all the shots and buyers were launching legendary bidding wars, waiving contingencies, and paying for homes in cash. But now, the shoe is on the other foot, and 92% of home sellers are accepting some buyer-friendly terms (frequently related to home inspections, financing, or appraisals), . . .”

This doesn’t mean we’re in a buyers’ market now, but it does mean you have a bit more leverage when it comes time to negotiate with a seller. The days of feeling like you may need to waive contingencies or pay drastically over asking price to get your offer considered may be coming to a close.

2. Sellers Are More Willing To Help with Closing Costs

Before the pandemic, it was a common negotiation tactic for sellers to cover some of the buyer’s closing costs to sweeten the deal. This didn’t happen as much during the peak buyer frenzy over the past two years.

Today, data suggests this is making a comeback. A realtor.com survey shows 32% of sellers paid some or all of their buyer’s closing costs. This may be a negotiation tool you’ll see as you go to purchase a home. Just keep in mind, limits on closing cost credits are set by your lender and can vary by state and loan type. Work closely with your loan advisor to understand how much a seller can contribute to closing costs in your area.

Bottom Line

Despite the extremely competitive housing market of the past several years, today’s data suggests negotiations are starting to come back to the table. To find out how the market is shifting in our area, let’s connect today.

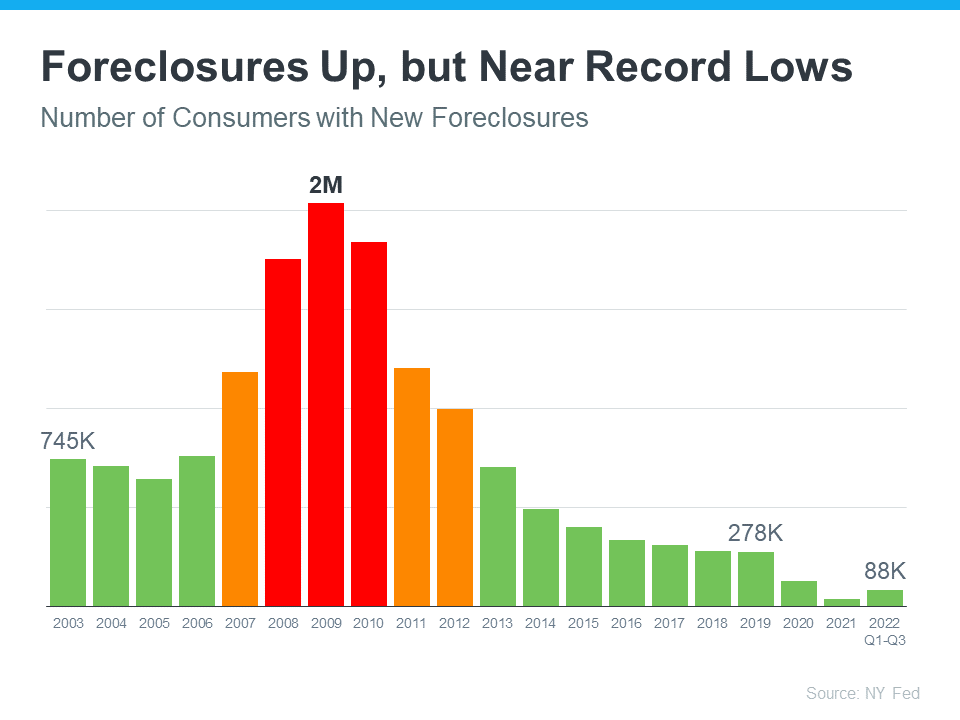

Why There Won’t Be a Flood of Foreclosures Coming to the Housing Market

With the rapid shift that’s happened in the housing market this year, some people are raising concerns that we’re destined for a repeat of the crash we saw in 2008. But in truth, there are many key differences between what’s happening today and the bubble in the early 2000s.

One of the reasons this isn’t like the last time is the number of foreclosures in the market is much lower now. Here’s a look at why there won’t be a wave of foreclosures flooding the market.

Not as Many Homeowners Are in Trouble This Time

After the last housing crash, over nine million households lost their homes due to a foreclosure, short sale, or because they gave it back to the bank. This was, in large part, because of more relaxed lending standards where people could take out mortgages they ultimately couldn’t afford. Those lending practices led to a wave of distressed properties which made their way into the market and caused home values to plummet.

But today, revised lending standards have led to more qualified buyers. As a result, there are fewer homeowners who are behind on their mortgages. As Marina Walsh, Vice President of Industry Analysis at the Mortgage Bankers Association (MBA), says:

“For the second quarter in a row, the mortgage delinquency rate fell to its lowest level since MBA’s survey began in 1979 – declining to 3.45%. Foreclosure starts and loans in the process of foreclosure also dropped in the third quarter to levels further below their historical averages.”

There Have Been Fewer Foreclosures over the Last Two Years

While you may have seen recent stories about the number of foreclosures rising today, context is important. During the pandemic, many homeowners were able to pause their mortgage payments using the forbearance program. The program gave homeowners facing difficulties extra time to get their finances in order and, in many cases, work out a plan with their lender.

With that program, many were concerned it would result in a wave of foreclosures coming to the market. That fear didn’t materialize. Data from the New York Fed shows there are still fewer foreclosures happening today than before the pandemic (see graph below):

That means, while there are more foreclosures now compared to last year (when foreclosures were paused), the number is still well below what the housing market has seen in a more typical year, like 2017-2019.

And most importantly, the number we’re seeing now is still far below the number we saw during the market crash (shown in the red bars in the graph). The big takeaway? Don’t let a headline in the news mislead you. While foreclosures are up year-over-year, historical context is essential to understanding the full picture.

Most Homeowners Have More Than Enough Equity To Sell Their Homes

Many homeowners today have enough equity to sell their homes instead of facing foreclosure. Due to rapidly rising home prices over the last two years, the average homeowner has gained record amounts of equity in their home. And if they’ve stayed in their homes even longer, they may have even more equity than they realize. As Ksenia Potapov, Economist at First American, says:

“Homeowners have very high levels of tappable home equity today, providing a cushion to withstand potential price declines, but also preventing housing distress from turning into a foreclosure. . . the result will likely be more of a foreclosure ‘trickle’ than a ‘tsunami.’”

A recent report from ATTOM Data explains it by going even deeper into the numbers:

“Only about 214,800 homeowners were facing possible foreclosure in the second quarter of 2022, or just four-tenths of one percent of the 58.2 million outstanding mortgages in the U.S. Of those facing foreclosure, about 195,400, or 91 percent, had at least some equity built up in their homes.”

Bottom Line

If you see headlines about the increasing number of foreclosures today, remember context is important. While it’s true the number of foreclosures is higher now than it was last year, foreclosures are still well below pre-pandemic years. If you have questions, let’s connect.

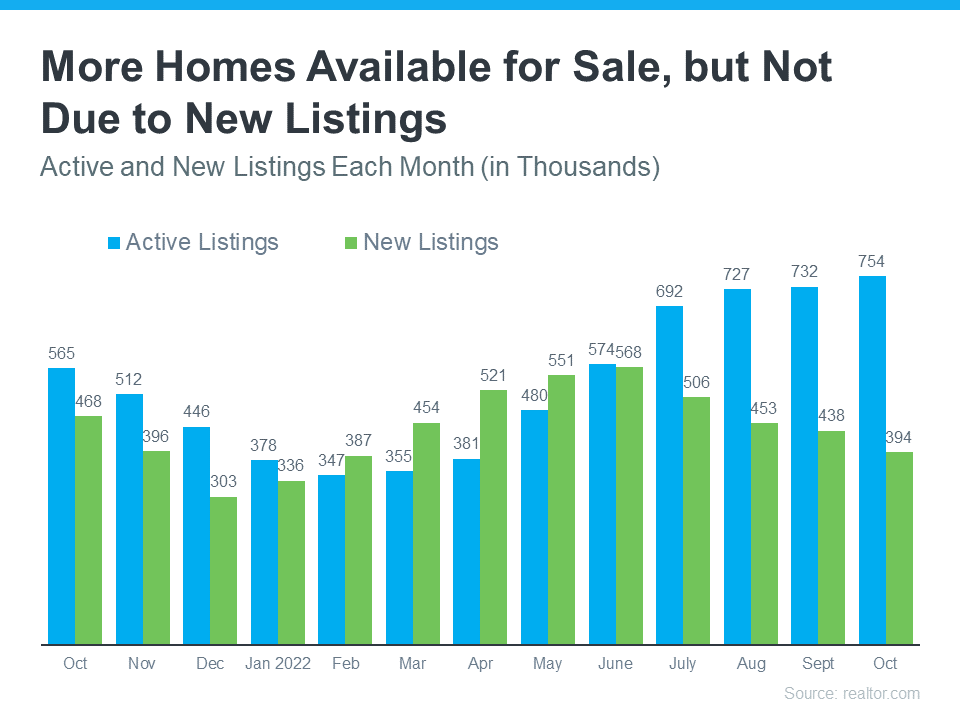

What Buyers Need To Know About the Inventory of Homes Available for Sale

If you’re thinking about buying a home, you’re likely trying to juggle your needs, current mortgage rates, home prices, your schedule, and more to try to decide if you want to jump into the market.

If this sounds like you, here’s one key factor that could help you with your decision: there are more homes for sale today than there were at this time last year. According to Calculated Risk, for the week ending in November 18th, there were 47.7% more homes available for sale than there were at the same time in 2021. And having more options for your home search may be exactly what you need to feel confident about making a move.

Here’s a look at where the increased housing supply is coming from so you can get a better sense of what’s happening in the market today and what it means for you.

What Caused the Growth in Housing Inventory This Year?

The increase we’ve seen in housing supply this year isn’t from the source you think it is. Rather than an influx of recent homeowners listing their houses for sale (known as new listings), the primary reason the supply has grown is because homes are staying on the market a bit longer (known as active listings).

That’s happening because higher mortgage rates and home prices have helped moderate the peak frenzy of buyer demand, which has slowed down the pace of sales. And, as the pace of sales has eased, inventory has grown as a result.

The graph below uses data from realtor.com to show that it’s active listings, not new listings, that have driven the growth we’ve seen over the past few months:

And while overall inventory gains may slow down this winter due to typical housing market seasonality, you still have a chance to capitalize on the current supply.

What This Means for Your Home Search

Regardless of the source, the increase in available housing supply is good for buyers. More homes available for sale means you have more options to choose from as you search for your next home, and you may even have more time to consider them.

So, if you tried to buy a home last year and lost out in a bidding war or just couldn’t find something you liked, this may be the news you’ve been waiting for. If you start your search today, those additional options should make it less difficult to find a home you love, especially as some other buyers pause their search this holiday season.

Just remember, housing supply is still low overall, so it won’t suddenly be easy – it’ll just be less challenging than it was at this time last year. As a recent article from realtor.com says:

“Despite this improvement in the number of homes actively for sale, active listings still lag their pre-pandemic levels.”

The increase in housing supply helps put you in a great position to kick off the new year in your dream home. And who better to help you find it than a trusted, local real estate professional?

Bottom Line

If you’re ready to jump into the housing market and see what’s available in our local area, let’s connect.